But to those of you who believed economic "experts" and commission-hungry tea-leaf readers who proclaimed 2009 was "the bottom" and planned to sell in a few years for profit...

WHAT THE HOLY HELL WERE YOU THINKING?

In addition to losers who bought during the bubble, I have documented quite a few 2008 buyers who purchased based on the false assumption that "the worst is over," and then faced total annihilation when they tried to unload just a few years later.

In addition to losers who bought during the bubble, I have documented quite a few 2008 buyers who purchased based on the false assumption that "the worst is over," and then faced total annihilation when they tried to unload just a few years later.

Well now I'm starting to see more 2009 buyers who believed all the bullshit about "the bottom" being in spring 2009 try to sell their "wise investments," only to learn that prices have fallen considerably since their supposed bottom.

And he's also undercutting his competition (another 2009 "bottom" buyer!) by $40,000, although that unit appears to be upgraded with granite, a new bathroom and plantation $hutters.

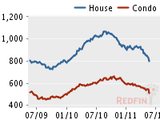

Very few people think about it, but because of commissions every seller is 6% underwater from the outset. That means if they hope to break even, home values would have to increase by a minimum of 6% during their ownership. For 2009 buyers operating under the premise that the last two years provided those kinds of gains, they are about to learn a valuable, and painful, lesson about the dangers of listening to those financially dependent on home price increases, instead of common sense and simple math.

That's because home prices on average have dropped by 5.1% since 2009. Welcome to the (totally foreseeable) double dip.

HAIL MARY ASKING PRICE: $429,900

1310 East OCEAN Blvd #803, Long Beach, CA 90802

BEDS: 1

BATHS: 1

SQ. FT.: 960

$/SQ. FT.: $448

VIEW: Catalina, City Lights, City, Coastline, Harbor, Marina, Ocean, Panoramic, Yes, White Water (Wait, it has a view of "Yes"?! Maybe this price isn't that bad after all)

YEAR BUILT: 1984

COMMUNITY: Downtown Area/Alamitos Beach

MLS#: S660918

ON REDFIN: 19 days

HOA FINE: $740 (OUCH)

1310 East OCEAN Blvd #803, Long Beach, CA 90802

BEDS: 1

BATHS: 1

SQ. FT.: 960

$/SQ. FT.: $448

VIEW: Catalina, City Lights, City, Coastline, Harbor, Marina, Ocean, Panoramic, Yes, White Water (Wait, it has a view of "Yes"?! Maybe this price isn't that bad after all)

YEAR BUILT: 1984

COMMUNITY: Downtown Area/Alamitos Beach

MLS#: S660918

ON REDFIN: 19 days

HOA FINE: $740 (OUCH)

DOWN PAYMENT: $86,000

MONTHLY NUT: $2,800

INCOME REQUIREMENT: $98,000/year

DESCRIPTION: Sleek and sophisticated luxury high rise with spectacular Ocean views from every room. This home is right on the beach. Ocean views by day and city lights by night. You ll never tire of seeing gorgeous sunsets or graceful sailing ships. Stunning home with modern kitchen and bath. Lots of sunlight spills through the floor to ceiling windows. Open floor plan, great for entertaining. Spacious master bedroom suite with walk in closets. Let the sound of the waves lull you to sleep. There are many amenities including 24 hour concierge, Fitness room and community room, pool, spa, cabana, BBQ area and fire pit. Conveniently located to downtown, shopping, restaurants, parks, museums, theater, Queen Mary, Marina and more!

DESCRIPTION: Sleek and sophisticated luxury high rise with spectacular Ocean views from every room. This home is right on the beach. Ocean views by day and city lights by night. You ll never tire of seeing gorgeous sunsets or graceful sailing ships. Stunning home with modern kitchen and bath. Lots of sunlight spills through the floor to ceiling windows. Open floor plan, great for entertaining. Spacious master bedroom suite with walk in closets. Let the sound of the waves lull you to sleep. There are many amenities including 24 hour concierge, Fitness room and community room, pool, spa, cabana, BBQ area and fire pit. Conveniently located to downtown, shopping, restaurants, parks, museums, theater, Queen Mary, Marina and more!

This fool bought in October 2009 for $420,000 (down from an original asking price of $450,000. He probably thought he was getting a smoking deal) and for whatever reason (oh, I don't know...maybe the obscene $740 HOA fine, the limitations of only one bedroom, or that he simply can't afford that monstrous monthly nut anymore) just 19 months later decided to lay his head on the chopping block--ERRR...put it on the market asking $30,000 more than he paid (anybody want to guess what the sales commissions are? Whoever said "around 30 Grand" wins a key chain).

He has since dropped the price to $430,000 in the hopes of that $10,000 cushion somewhat offseting what is sure to be a sizable hit to his finances...but things aren't looking good.

On a positive note, the views are astounding:

The interior looks largely untouched from the 1984 build date (the dead giveaway is the florescent overhead lights in the kitchen and those gnarly bathroom counters), but you're mostly paying for the view in these types of places anyway.

And more good news: There is a sold comp from a few months ago that sold for $475,000 (but if that comp really was indicative of fair market value, then why would our seller need to reduce his original $450,000 asking price? Hmmm).

And he's also undercutting his competition (another 2009 "bottom" buyer!) by $40,000, although that unit appears to be upgraded with granite, a new bathroom and plantation $hutters.

The overall point is that he's just $9,000 above his 2009 purchase price and there still doesn't appear to be any interest. Which means more price cuts. Which means he is about to be in a world of hurt.

Let's put it this way, with 10% down ($42,000), after $27,000 in commissions and $14,800 in HOA fees, all of that down payment money is now gone. POOF!

If he put 20% down (likely, given how panic-stricken 2009 was), he's now halfway through that money. And every additional price reduction just eats further and further into that former nest egg of his.

Sure, he'll have some equity after 19 months of payments, but not nearly enough to break even on this foolish purchase. The question is not if he will lose a great deal of money on this, but how bad the damage will be.

His biggest challenge will be finding a wealthy, single, retiree who is financially savvy enough to be able to afford this place, but dumb enough to believe there will not be better buying opportunities in the future. Yeah, good luck with that.

However, there are some who say there won't necessarily be any better deals in the future because all of the must-sell inventory has been washed out of the market, the Fed can keep interest rates low and banks can keep supply off the market for as long as it takes, thus keeping supply artificially restrained and prices from falling. And maybe they're right (of course, if they were then we would have never entered the double dip in the first place, but I digress).

Maybe the banks and Fannie/Freddie and FHA can indeed keep their massive pools of inventory off the market for years or decades and interest rates will hover under 5% for years to come (they've certainly pulled it off so far).

But suppose just for a moment that they can't pull it off. If interest rates rise by 1 or 2%, or supply increases by 15 or 20% -- or both -- what effect do you think that will have on prices? Until we are in a more normal market with real inventory and serious sellers, nobody -- and I mean NOBODY -- can be confident in their predictions of 2011 (or 2012, 2013, or 2014) being the true bottom (just like they were all wrong in '08, '09, and '10)

Here's the bottom line: If you are buying a place right now because you are confident you will be there for 10 years or longer and your finances and job are reasonably stable, then go for it. The Rent vs. Buy equation has become a no-brainer in most areas by now and these rates are incredible.

But if you think there's even a remote chance that you'll need to sell in the next few years, renting would be the most logical choice (if nothing else than for mobility's sake). Property values have likely seen the last of the big, gut-churning drops, but that is very different than a resumption of gains. And considering you'd be 6% underwater from day one, if you needed to sell in 2013 there's no way you'd get out for break even.

Yes, a home can be an investment, but it is also an expensive consumer good that must be viewed as a liability. If you don't believe me, why don't you ask the seller of this apartment which of the two he believes he bought.